Your money mindset defines how you think about money and influences how you save, how you spend, and how you manage your debt. It’s your core beliefs about money and your attitude towards it.

This includes:

- What you think you can and cannot do with money

- How much money you think you deserve

- How you believe you should manage your money (spend, save, share)

- How you believe you should manage your debt

- Your ability to grow your wealth

- Your overall financial confidence

Importance of a Positive Money Mindset

The importance of money in reaching financial success cannot be overstated. Your daily and long-term financial decisions and results can be greatly influenced by your attitudes, beliefs, and perceptions around money. There is much more to having a healthy money attitude than just knowing the basics of finance. Everyone needs to have one.

A money mindset is quite simply your attitude about money and your unique set of beliefs about financial matters. Your money mindset affects how you think about finances, how you plan, how you deal with setbacks, how you save and spend, and how you deal with debt.

Understanding the kind of money mindset you have is powerful. It can help you figure out the best way to meet your financial goals, and be aware of possible pitfalls, obstacles and challenges. “It is very important to acknowledge your money mindset; to understand how you approach money, spending, and saving. It will help you to understand what you may need to tackle to achieve longer-term goals,” says Stuart Gray, director of RBC’s Financial Planning Centre of Expertise.

Your money mindset is shaped by many factors. Some factors are your upbringing, cultural influences, personal experiences, and social conditioning. Intentionally or unintentionally, these factors determine your beliefs about money, abundance, scarcity, and your worthiness to attain financial success.

Table of Content

- Understanding Your Relationship with Money

- Building a Positive Money Mindset

- Goal Setting and Financial Planning

- Investing in Financial Education

- Overcoming Financial Challenges

- Navigating Social Influences and Peer Pressure

Understanding Your Relationship with Money

When it comes to money, everyone has complicated relationships. The upbringing you had regarding money and morals as a youngster and the way you processed this knowledge mentally are the two main influences on how you earn, spend, and handle money. For instance, you might tithe to the church if you appreciate religion. You may also make college savings your top priority if you value education.

This is a spectrum relationship with money. There are two extremes to financial insecurity. On the one hand, you can be exceedingly thrifty and worried about how little money you have; on the other hand, you might be reckless. The way each of us processes and organizes money messages—as well as the ways in which we model money behaviors—is unique.

Developing a Financial Style

We are bombarded with messages about money from toddlerhood to adulthood. Even individuals who are raised in the same household do not necessarily have the same view about money or their relationship with money. And, although you may develop your financial style early, it can change over time or due to circumstances.

It’s not uncommon for someone who’s undergone a significant life change to adopt a very different relationship with money. For instance, if you have a near-death experience, you may abandon the “saver” mentality and instead spend on experiences to make the most of your life. Similarly, the birth of a child may inspire you to save for the future.

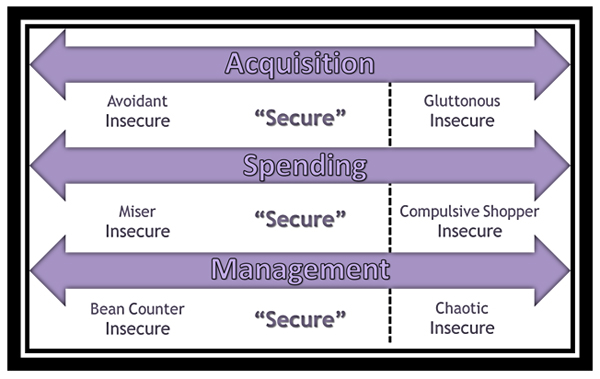

Following is a discussion of the three dimensions of money. Typically, the dimensions are unequal in importance—you may place a higher value on acquisition than management. When evaluating these dimensions, think about where you fall on the spectrum. How can you improve your relationship with money?

Dimension of Acquisition

The dimension of acquisition deals not with how you acquire your wealth, but with how much money is necessary for you to feel secure. Some people believe that money is the “root of all evil;” others believe that you can never have enough. Still, there are some individuals who find the acquisition of money to be an irrelevant pursuit. When it comes to acquiring money, you may be avoidant, insatiable or somewhere in between. Where do you stand?

In the extreme, an individual may bend rules, or even break the law, to acquire more money. Even people of considerable means can fall prey to the idea that “you can never have enough.”

Dimension of Spending

Once you have acquired money, there’s the question of “what do you do with it?” Most of us have heard stories about individuals who “penny-pinch” their whole lives and die with a considerable sum in the bank. Or, you hear of star athletes who make millions over the years, only to end up with nothing.

On one end is the miser; on the other end is the compulsive spender. Most of us are reasonable, careful and intentional with how we spend money; however, sometimes, we experience episodes where our spending is “out of control.”

Dimension of Management

The compulsive spender is often a poor money manager. But like your acquisition and spending habits, the way you manage your money is highly individualistic.

Money management covers everything from how you pay your bills to how you manage your investments. The micro-manager must account for every nickel and dime, while the person who is completely disorganized with money may procrastinate when paying bills and be unaware of the true condition of his or her finances.

Money relationships at either end of the spectrum are generally detrimental—you must find a healthy balance. A “normal” or “secure” relationship with money means that your acquisition, spending, and management styles will not cause financial difficulties and that you are reasonably content with the relationship. If you have an “insecure” relationship in one of the money dimensions, then that relationship has already gotten you into money trouble or it may yet do so.

After you determine where you fall on the spectrum, you can focus on changing unhealthy money habits or reinforcing healthy ones. The Center for Health offers resources to help you find, or keep you in, financial balance on the Financial page on the Center for Health website.

Strategies for Changing Negative Money Perspectives

Your money mindset is formed from your distinct lived experiences. Everyone has a different story and relationship with money because everyone has had different experiences with it throughout their lives. Someone who worked during high school and college might have a different perspective on saving than someone whose first job was well into their 20s.

Along with your personal experiences, your mindset is also formed by how money impacted the people closest to you.

- Was money a taboo topic in your house?

- Were your parents or loved ones constantly stressed about money?

- Did your family prioritize charitable giving?

- Was financial literacy a core topic of conversation in your house?

All of these past experiences likely influence your attitude and approach toward money today. Someone who grew up in an environment where money was a sore spot might not like managing their finances (or might always worry about having enough money to support themselves and their family).

Your attitudes and perspectives are shaped by the people around you, and those closest to you tend to profoundly influence your thoughts and beliefs. As the saying goes, you are who you spend time with,

Check out the table below for characteristics of bad and good money mindsets:

| Bad Money Mindset | Good Money Mindset |

|---|---|

| Fear and anxiety Feeling a lack of control Negativity around the concept of money Feeling intimidated by difficult concepts Defeatism (“I’ll never be good at this”) Procrastination (“I’ll get to it eventually”) | A willingness to tackle difficult problems Feeling in control of behaviors and decisions General optimism in the face of uncertainty Openness to learning new things Solution-oriented attitude Acknowledgement of incremental progress |

Your money mindset is directly connected to your current financial habits. It affects how you approach money, the way you view and use debt, how you think about your future, and how you view the financial habits of others.

When you know how you approach money, you’ll be more equipped to make intentional decisions that push you in a positive direction. After reflecting on this concept, you may realize you lean on your credit cards too often for purchases you don’t need and that don’t further your goals. You may also discover your propensity for giving comes from a long line of generous role models.

Read Also: The Art and Science of Wealth Accumulation: Strategies for Financial Prosperity

Your money mindset also reveals both your positive and negative traits regarding financial management. This concept isn’t inherently intuitive. It’s critical to spend some time thinking through these questions and being honest with yourself about your attitude toward your money.

The best thing about a money mindset? Like perspectives, they can shift. Here are a few ways you can change your mindset to improve your financial outlook.

Personal finance is subject to change and fluctuation, meaning there’s always space for improvement. Recall that you have influence over your financial thinking. The following are some strategies for progress and evolution:

- 1. Believe You are Destined and Deserve Success

Too often, a negative mindset leads people to give up on their financial goals. It’s important to approach your money from a place of openness, curiosity, and excitement. Believing that you can reach your goals and find success is the first step. Once you have that foundation, you’ll be able to construct habits that support those beliefs.

This doesn’t mean your entire financial road will be paved with rainbows and sunshine, but it does mean you’ll allow yourself to find success. How can you shift this perspective? Spend some time setting new financial goals. Your goals are the foundation of your financial plan. Once you have your goals, set some key milestones to celebrate as you work toward them.

Starting from a positive headspace will help you make choices that are aligned with those productive thoughts.

- 2. Picture Your Future Self

Sometimes it’s crucial to flip this tough interview question back on yourself. Where do you see yourself in 5, 10, 20, even 30 years? Where have you grown? What have you accomplished? What do you want for your future self? Picturing your future can be a telling exercise as it can reveal if you’re on the right path to attaining it.

Maybe starting your own business is a critical milestone in your life. You might suddenly realize you haven’t started saving for this venture or really thought about the type of business for you. Fill in those missing pieces so you can set yourself up and bring that future vision to life.

You might also try picturing your dream retirement. Where are you living? How are you spending your time? Are you fulfilled? When you can see your future self, you can find the motivation you need to get there. Maybe this year commit to maxing out your retirement accounts or increasing the contributions to your other investments.

- 3. Give Freely and Generously

Your comfort level with giving back to causes, organizations, and people you care about says a lot about your money mindset. In general, those who intentionally make space for giving feel more confident, secure, and fulfilled with their money.

Every person will have a different capacity for giving, but when you feel comfortable giving away some of your money, you’ll move from a space of scarcity to one of abundance.

A scarcity mindset is a dangerous narrative, one that leaves you constantly chasing the idea of “enough”. Abundance, on the other hand, is about setting yourself up for financial success and structuring your money in a way that brings meaning and fulfillment.

- 4. Immerse Yourself in Knowledge

One of the best ways to combat negative habits is to learn healthier ones. Financial management isn’t simply intuitive, it’s something you need to work toward and spend time with to get right.

- Take some time to read books, blogs, and articles. These resources can broaden your perspective and help you improve the areas where you’re struggling.

- Talk with family and friends about the questions you have. They might be able to share their wisdom or perhaps just open a line of conversation.

- Seek out a professional. A financial advisor can help address your money mindset and give you practical tools to improve it.

Knowledge is power and making the most of the resources available to you will help you shift your perspective.

- 5. Know Where You Are and Where You Want to Be

To change something, you need to understand two elements:

- Where you are.

- Where you want to be.

Let’s use investing as an example. When you know you veer into a scarcity mindset when the topic of investing comes up, you can use the tools and resources around you to overcome those feelings. If you want to reach your financial goals, odds are you’ll have to embrace investing.

To embrace the role investing plays in your finances, do some research on what investing means to you. Understand your risk tolerance, set goals, and work with someone you trust. All of these elements will help you build a positive and fulfilling mindset.

Building a Positive Money Mindset

Even if there’s no getting around the difficulties that many of us are currently facing, there might be some tactics we can employ to foster a more optimistic outlook on money when the cost of living is rising.

Visualize Success

What works for athletes and other highly successful people can also work for you and your money habits. Visualizing accomplishments is the first step in creating a positive money mindset and achieving financial well-being.

Here are some things you can envision before actualizing:

- There’s a four-figure balance in your savings account … and it’s growing!

- Your highest-interest credit card is paid off — that zero balance is going to feel amazing!

- You have extra money at the end of each month to be charitable.

- A comfortable retirement will be a reality because your 401(k) balance is growing with your contributions and the maximum employer match available.

- There’s money each month for self-care so that you can get your nails done, play a round of golf, or even buy simple things like a new bath bomb or scented candle to enjoy at home.

- You’re on vacation at a beautiful resort that you saved and paid for in full.

Focus on the fact that this crisis will pass

History shows that, given time, today’s economic woes should eventually be overcome. Most periods of history have experienced enormous challenges, ranging from great depression and pandemics to a global financial crisis. All have passed, and life has carried on, but they may have felt all-consuming at the time as people struggled to manage their lives and the impact on their finances.

At present, we are facing high inflation and a cost of living crisis, amongst other things, however, the Bank of England has said that inflation is expected to fall back towards its 2% target within three years as the impact of Covid and conflict in Ukraine diminish.

Things are starting to ease, and inflation fell to a two-year low of 4.6% in the 12 months to October. In the Spring Budget, Chancellor Jeremy Hunt revealed forecasts from the Office for Budget Responsibility that said inflation is expected to fall to 2.9% by the end of the year.

Accept uncertainty

None of us can say for certain what’s going to happen tomorrow, or next year in the world economy. The past few years have proved extraordinarily challenging, and it’s often natural to fear the worst. However, it’s important to accept that uncertainty is a fact of life.

In fact, the only certainty is that things can and will change over time. Knowing that you’re not alone in struggling with uncertainty, and accepting that very little in our lives is certain can be helpful in coping with anxiety, whether about your finances or other aspects of your life.

Maintain and develop positive habits

You may be forced to stop saving or investing for your future to make ends meet, but if you are fortunate enough not to be in this position, beware that stopping contributions to pensions and ISAs could prove an expensive mistake in the long term.

One of the basic principles of investing towards retirement is to put your money to work as soon as possible. Investments, whether they be stocks and shares, bonds, property or cash, need time to grow, so the longer you leave your money invested, the more chance you have of making gains. Also, by drip-feeding your money into your pension on a monthly basis, you buy more shares when their price is low, and fewer when they rise in value. This can help to smooth out volatility, and mean that you effectively pay the average price for your investment over time.

Another positive habit that’s worth maintaining or developing is regularly reviewing your bills, budget and spending habits. This may seem stressful when the cost of living is soaring, but making this part of a monthly routine can give you a sense of control over your finances and help you to feel more positive.

Focus on your goals

You may be tempted to react to short-term market volatility by selling your investments in your personal pension or stocks and shares ISA. However, this only serves to cement losses and means you’ll potentially miss out on gains when markets eventually recover. After all, as the old adage goes, it’s about time in the market, not timing the market, when it comes to long-term gains.

To avoid making any knee-jerk reactions as a result of what’s going on, try to focus on your long-term financial goals, such as living comfortably in retirement, or saving for your children’s higher education. If you are thinking of changing something in particular, such as selling an investment that’s sunk in value, ask yourself whether this approach helps you to meet your goal. If the answer is no, then this could be a sign that your decisions are being influenced by what’s going on in the world in the short term rather than your personal goals and your approach to risk.

Meanwhile, it’s worth noting that if your goal is to build a savings buffer, now is a good time to see if you can get a better deal elsewhere on your cash as interest rates are rising. Check savings websites such as SavingsChampion.co.uk or price comparison sites such as Moneyfacts.co.uk, or uSwitch.com to see if you can find an account paying higher returns to move to.

Make the most of available help

It’s more important than ever to check you’re getting all the financial help you’re entitled to, and by doing so, you’re taking a positive step toward improving your financial situation.

Fortunately, there has been some positive news recently with Chancellor Rishi Sunak announcing that the October discount on energy bills will be doubled to £400. The requirement to pay back this payment, which will be spread over six months, has been scrapped. More than eight million low-income households on benefits such as Universal Credit, Tax credits and legacy benefits will receive a one-off £650 payment on top of the £400 payment.

It’s simple to check if you might be able to claim benefits. Try one of the online benefits calculators such as those provided by Entitledto.com and Turn2us. You’ll need to provide details of your income and any savings, as well as how much you spend on major outgoings such as your rent or mortgage.

If you don’t qualify for additional support with energy bills because you aren’t in receipt of benefits, you may still be entitled to money off your bills under the Warm Home Discount scheme. This is a one-off discount on your electricity bill paid on your behalf to your energy supplier between September and March.

A further cost of living payments will be made this year. In 2023-24, those receiving means-tested benefits will receive £900, pensioner households will receive £300, and individuals on disability benefits will receive £150. The £900 payment follows a £650 grant for people in receipt of means-tested benefits that was paid in two installments last year. For those eligible, payments will start in the spring and be made in three installments.

Build your understanding

Instead of focusing on negative headlines, a worrying economic period can actually be a good time to develop your general understanding of how best to manage your money.

If you’re aged 50 or over you can receive free guidance from the Government’s Pension Wise service on your choices at retirement. Call them on 0800 138 3944 to book a free appointment, or you can book through their website.

If you’re considering getting professional financial advice, Aviva is offering Rest Less members a free initial consultation with an expert to chat about your financial situation and goals. There’s no obligation, but if they feel you’d benefit from paid financial advice, they’ll go over how that works and the charges involved.

Find expert inspiration

Take a deep breath and remember that feeling anxious about your finances is entirely normal, especially during these difficult times, but that it’s also easy to lose perspective. However, decisions made when emotions are running high are rarely good, and often the best way to be successful with your money over the long term is to tough it out.

Taking note of what professional investors say to achieve long-term gains may help you to keep a cool head when there’s stock market turbulence. Here are some quotes you might find useful:

“The best way to measure your investing success is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go.” – Benjamin Graham

“Close the doors. Be fearful when others are greedy. Be greedy when others are fearful.” – Warren Buffet.

“Courage taught me that no matter how bad a crisis gets…any sound investment will eventually pay off.” – Carlos Slim Helu.

Share your concerns and seek help

Part of cultivating a positive money mindset is being comfortable enough with family and friends to share your worries, and that includes any concerns you have about your finances. Spiraling living costs are a concern for all of us, and it can be a relief to get any concerns out in the open.

For example, you may have particular concerns about debts. The last few years have placed huge financial pressure on many of us, and if you were already struggling with debts, staying on top of these can be really stressful. It may seem that they are impossible to deal with, but sticking your head in the sand will only make matters worse.

Fortunately, there is plenty of help available from a variety of charities and organizations if you’re having difficulty managing repayments and are worried that you won’t manage to repay your debts. For example, get in touch with Citizens Advice on 0800 144 8848 (England) or 0800 702 2020 (Wales), or StepChange on 0800 138 1111 if you need someone to talk to.

Goal Setting and Financial Planning

To attain financial freedom, one of the most crucial parts of financial planning is setting clear, meaningful goals. Simply said, financial goals are targets that are determined by our desired timeliness and future financial demands.

A major issue with financial planning is that, although most of us understand the need of goal-setting, we still devote a significant portion of our time to analyzing our current financial status and little to no time to creating future objectives. Setting goals, though, is a crucial step in the investing process and needs to be done carefully.

Goal setting is important for many reasons:

Goals allow creating a realistic planIf you have a well defined goal then it allows you to create a plan which is realistic in nature. Your financial goals can be anything like wanting to pay-off debt, saving up for children’s education, retirement etc. Once you have your goals in place, you will plan and save accordingly to achieve it. For example, you wish to accumulate a corpus of Rs.1 crore before retirement then you exactly know how much you have to save and for how long in order to achieve this goal.

Goals give direction to investments

Goals give direction to your investments. Clearly defined goals provide a purpose to your investments and help you stay focussed and curb unnecessary expenditure so as to achieve those goals in the long-term.

Goals help prioritise

Like all situations in life, financially too, we are pulled in many directions. There is a lot we wish to achieve but at the same time we have we cannot do it all at the same time. However, creating financial goals helps us prioritise us for the short and long-term.

Goals help stay disciplined

One of the most important things in investments is that you should be disciplined about it. When you are investing for a specific goal and monitor your progress then it acts as an incentive and helps you to stay disciplined..

Goals help create accountability

When you establish specific financial goals you your focus and hold yourself accountable. Clearly defined goals to be achieved in future help create accountability. Whenever you write down a specific goal and work towards it you continuously monitor your progress and are honest about it. You get into the habit of reviewing your progress and are honest about it which helps you stay on the right path.

Goals give a sense of achievement and help celebrate your accomplishment

All of us like to get rewarded for our efforts. Creating financial goals and achieving them are the rewards of your goal based investments. These significant milestones provide you with a sense of achievement.

How to set goals for yourself?

Setting goals for your future planning is not a difficult process and can be done by keeping these few important things in mind:

- Pen down your goals: Once you have written down your financial goals, you can prioritize them in order of importance. If you are one of those who love making list to do things and then striking them off, achieving financial goals and crossing them off will be very satisfying.

- Your goals should be S.M.A.R.T.

- Specific- Each goal should be specific and clearly defined

- Measurable- Set measurable financial goals so as to know when you have reached it.

- Achievable- Your financial goal should be practical and well within your financial reach.

- Relevant- It should be relevant to you.

- Time-bound– Each goal should be time-bound so that you can monitor your progress and achieve it within a desired time frame

- Make a plan of action After defining your goals make a list of things that you need to do in order to achieve these goals.

- Review your goals Once you have set your goals and are working towards it, it is equally important that you are continuously reviewing them from time to time. This will help you to stay on track.

Here are some more of the most common financial goals people set and tips for making them happen. Are any of these on your list?

- 1. Create and stick to a budget.

Not only is budgeting one of the top financial goals people set each new year, but it’s also the foundation you should build all your other money goals on.

A budget is how you make progress with your money. It’s a plan for what’s coming in (your income) and what’s going out (your expenses). You’re telling your money where to go instead of wondering where it went. When you have this plan for your money, you can feel confident you’re taking steps toward your goal every month.

Budgeting helps you gain momentum in every area of your finances.

- 2. Build up an emergency fund.

Life happens. But you can be prepared for any money problems that come your way if you’ve got enough money saved up. I’m talking car trouble, medical expenses and busted toilets (you know, some of the most inconvenient parts of being an adult). But when you’ve got an emergency fund, you can rest well at night knowing you won’t have to go into debt to cover those moments.

Start with the financial goal of having $1,000 in savings. Then, if you have debt, it’s time to knock that out. After that, you want to build up a fully funded emergency fund with 3–6 months of expenses.

When you’ve got an emergency fund, you’re ready for those “life happens” moments. Instead of being worried about what could happen next, you’ll feel confident that you’ve got money set aside to deal with it.

- 3. Get out of debt.

If you’ve got debt, it’s time to get serious about paying it off. All of it. Yeah, I know that may seem impossible right now, especially if you’ve got some big numbers staring you in the face—student loans, credit cards, whatever makes up that debt. But here’s the ugly truth: Debt doesn’t move you forward. It holds you back. You can’t get ahead with your money if it’s always going to lender payments.

- 4. Save up for your dream retirement.

Let’s take a second to put on our imagination caps and picture the ideal retirement. Maybe that’s five, 10 or 30 years down the road. Do you want to pack up the grandkids and head to Disney every Christmas? Visit a new state with your spouse once a quarter? Stay home and read every book on your shelves? Take up a fun hobby or travel for international cooking lessons?

No matter what you’re dreaming for the future, you’ll need good retirement investments now to make it a reality. After you’re debt-free and have a fully funded emergency fund, I want you to start investing 15% of your household income for retirement. And guess what? When you have zero debt, all that money you spend on payments can go straight into your accounts to fund your retirement dreams.

- 5. Spend less and save more.

Tons of people whip goals out of the air, like “I want to spend less” or “I want to save more,” without thinking about what it means to actually do those things. People, you’ve got to be specific with your goals and intentional about your money habits.

Becoming successful with money is more about changing your behavior than anything else. This can look like creating and sticking to your budget every month, finding deals, using coupons, paying cash, and making more money. And here’s a big one: You’ve got to learn how to say no—even to yourself. I’m not saying never have fun. But if you want to save money, it’s going to take some planning and lifestyle adjusting.

Investing in Financial Education

The capacity to comprehend how funds function and how to manage them well is referred to as financial education. It entails developing good money management skills as well as financial planning, investing, saving, and making wise financial judgments. A higher quality of life can result from making wise financial decisions, which are made easier with the assistance of financial education.

For a number of reasons, financial literacy is essential to both career and personal success. It first gives a clearer grasp of the operation of money, investments, and the financial system. Secondly, it facilitates the process of making wiser financial decisions, which can result in increased prosperity and financial stability. Thirdly, it offers the groundwork for constructing a strong financial future, which can boost confidence and stability.

To better understand the importance of financial education, it’s useful to look at some of the challenges faced by people who lack it. First, they may have difficulty managing their money effectively. This can lead to a lack of savings, increased debt, and not being prepared for financial emergencies. In addition, they may miss valuable investment opportunities due to a limited understanding of the financial market.

Second, lacking financial education can make it difficult to make important career and business-related decisions. For example, it can be difficult to know when it’s the right time to change jobs or start one’s own business. Likewise, not understanding how business finances work can hinder the success of a business.

Finally, lacking financial education can affect self-confidence. Without the ability to manage money effectively and make important financial decisions, it’s easy to feel insecure and less than capable. This can have a negative effect on your personal and professional life.

Because it impacts everyone, regardless of age, wealth, or financial status, financial education is essential. To make sure we’re making wise choices and avoiding costly errors, we all need to be financially literate. The following justifies the need of financial literacy for both career and personal success:

The Importance of Understanding Financial Concepts

- It allows you to make better decisions

Having the necessary information helps you make informed decisions about your finances. This means you can assess your current situation, set goals, and create a plan to achieve them. If you have a clear understanding of your finances and how they work, you can make smarter decisions and avoid impulsive decisions that could negatively affect your financial situation.

- It helps prevent debt and financial problems

Financial education also helps keep you from accumulating debt and other financial problems. If you have a clear understanding of how to manage your money, you can avoid taking out unnecessary loans or spending more than you earn. You can also establish a budget and a plan to reduce your existing debts, which can improve your ability to obtain future loans.

- It helps you save and plan for the future

Controlling your expenses also helps you save and plan for the future. If you understand how to invest your money and make it grow, you can build an emergency fund and save for long-term goals, such as retirement or your children’s college education. In addition, you can learn about the different types of investments and how to choose the best ones for your financial objectives.

- It improves your quality of life

Improving your quality of life is one of the most important reasons why financial education is key to personal and professional success. When you understand how to manage your finances effectively, you can take steps to ensure that your life is more comfortable and fulfilling.

One of the ways financial education can improve your quality of life is by helping you avoid unnecessary debt, which can be a huge problem that can affect your quality of life. If you have too much debt, you can feel stressed and overwhelmed, and it can be a difficult situation to get out of. Financial education can teach you how to manage your finances effectively, including how to manage your income and expenses to avoid accumulating debt.

When you know how to manage your money, saving becomes more important, which can allow you to achieve your long-term financial goals, such as buying a home or a car, or even planning for retirement. Saving can also help you deal with unforeseen circumstances, such as medical emergencies or unexpected expenses.

- It helps you negotiate and get better deals

This knowledge can help you negotiate and get better deals. If you understand how finances work, you can evaluate options for loans, credit cards, and other financial products and choose the best option for your needs. You can also negotiate lower rates and interest rates if you have a clear understanding of how these financial products work.

- It allows you to be more independent

Financial education also allows you to be more independent. If you know how to manage your money, you don’t need to rely on others to make important financial decisions. This can allow you to make decisions more effectively and avoid situations where others may take advantage of you.

- It prepares you for unforeseen circumstances

By understanding how to save and manage your money effectively, you can be better prepared for situations such as job loss, illness, accidents, or other financial emergencies. Having an emergency fund and knowing how to manage your money in difficult situations can help you overcome these difficulties more easily.

Recommended Books, Courses, and Resources

The majority of people discover personal finance comparatively late in life. However, college students and new graduates can put themselves on the path to a better financial future by taking charge of their finances early on. Acquiring knowledge of personal finance will assist you in swiftly eliminating debt and releasing additional funds for vacation, real estate, investments, and other financial objectives.

Some of the top books on personal finance for college students are included in the list below. These books can assist readers in overcoming debt, including student debts, creating and maintaining healthy financial habits, and selecting wise long-term investments.

- Broke Millennial: Stop Scraping By and Get Your Financial Life Together by Erin Lowry

Everyone has to start somewhere. Even if you’re relatively new to the financial scene, there are tons of quality books to help teach you everything you need to know. Yet, Erin Lowry’s book, Broke Millennial: Stop Scraping By and Get Your Financial Life Together, stands apart from the rest.

Lowry’s simple, conversational tone is certainly helpful, as she walks you through the basics of budgeting, picking the best bank for you, dealing with debt, preparing for retirement, and more.

- Bye Student Loan Debt: Learn How to Empower Yourself by Eliminating Your Student Loans by Daniel J. Mendelson

Author Daniel J. Mendelson and his wife once had nearly $150,000 of student loan debt due to many years of graduate school and hefty interest rates. By creating and sticking to a simple repayment process, the couple became debt-free within five years.

In Bye Student Loan Debt, Mendelson walks you through his simple debt repayment system. And more importantly, the book will give you hope if you are feeling like you’ll never pay off your student loans.

- 365 Ways to Live Cheap: Your Everyday Guide to Saving Money by Trent Hamm

Frugality is one way to fix your financial situation. By living on the cheap, you have more money for the things that are truly important to you.

Trent Hamm, founder of the blog The Simple Dollar, knows how to be frugal. Hamm credits frugality and mindfulness for overhauling his formerly dire financial situation. And, his book, 365 Ways to Live Cheap: Your Everyday Guide to Saving Money, offers some easy ways to save money in your day-to-day spending.

- The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns by John C. Bogle

The Little Book of Common Sense Investing is the classic guide to getting started with the stock market. And, while you may not recognize the author by name, you certainly know of him – John C. Bogle is the founder of the investment company Vanguard. Bogle believes investing is for everyone, regardless of your education, income or experience.

While the stock market has its ups and downs, Bogle’s book has withstood the test of time. It is now on its tenth-anniversary edition.

- Hustle Away Debt: Eliminate Your Debt by Making More Money by David Carlson

While most financial books focus on saving, Hustle Away Debt offers a fresh perspective by teaching you about the importance of increasing your income.

Author David Carlson is also the founder of the popular millennial financial blog Young Adult Money. In his book, he details his secrets to getting out of debt by increasing his income through side hustles. If you’ve ever wanted to increase your income while learning new skills, then this book is a must-read.

- The Money Book for the Young, Fabulous & Broke by Suze Orman

Suze Orman is one of the original financial gurus. She has seven New York Times bestsellers, but you may recognize her most from her television show, The Suze Orman Show.

Orman provides to-the-point, no frills financial advice. For those just learning to budget (or learning to stick to a budget), look no further than The Money Book for the Young, Fabulous & Broke. Orman walks you through everything you need to know.

- Money Talks: The Ultimate Couple’s Guide to Communicating About Money by Talaat and Tai McNeely

Relationships and money are often a neglected topic. In fact, in a study by CreditLoan.com, over 30 percent of men and women hid a financial secret from their partners.

To say there is room for improvement is an understatement. That’s where Money Talks: The Ultimate Couple’s Guide to Communicating About Money comes in. This book hits on a sometimes sensitive topic. Not only does it provide valuable communication tips, but it teaches you how to set and achieve financial goals as a couple.

- Total Money Makeover by Dave Ramsey

Dave Ramsey is one of the top financial writers out there. His book, Total Money Makeover, shows you how to take control of your finances in a simple 10 “baby-step” process, which includes paying off debt, saving for an emergency fund, starting to invest, and other financial goals.

Total Money Makeover provides foolproof, no-nonsense advice for anyone looking to improve their financial situation.

- Rich Dad Poor Dad: What the Rich Teach Their Kids About Money – That the Poor and Middle Class Do Not! by Robert T. Kiyosaki

In the book Rich Dad Poor Dad, author Robert Kiyosaki outlines the lives of two men: his father, who was constantly broke, and his father’s friend, a wealthy entrepreneur. He believes “street smarts” can often be more valuable than a more traditional education.

Rich Dad Poor Dad challenges the conventional ideas of saving by providing information on how your current view of money can affect your future finances.

- How to Retire Early: Your Guide to Getting Rich Slowly and Retiring on Less by Robert and Robin Charlton

At the age of just 43, Robert and Robin Charlton were able to retire from their full-time jobs. They had worked a collective total of just 15 years. They now run a website, WhereWeBe.com while traveling the world.

Their book, How to Retire Early: Your Guide to Getting Rich Slowly and Retiring on Less, is designed to help others do the same thing they did. They outline repeatable steps that anyone with a full-time job can implement. Overall, they aim to communicate that retirement is not just a dream. It’s achievable.

Overcoming Financial Challenges

Numerous customers are facing financial strain as they attempt to safeguard their finances, make future plans, and simply make ends meet. This stress stems from a variety of factors, including recent high-profile bank failures, extremely high inflation, and fears of a recession.

In fact, according to Bankrate’s 2023 Money and Mental Health Survey, over half (52 percent) of Americans believe that money occasionally or frequently has a negative impact on their mental health. Of those who are affected by financial concerns, over one-third (29%) worry on a daily basis.

Even while outside circumstances are frequently to blame for financial stress, there are activities you can take to increase your financial stability and reduce it.

Below we’ll show you how to overcome financial problems and difficulties and ease your stress.

1. Identify the Underlying Problem That’s Causing the Difficulties

The first step to overcoming financial problems is to identify the underlying issue that’s causing the financial difficulties. Financial problems are usually a symptom of a bigger issue. To come up with solutions that work in the long run, take the time to identify the real source of your financial troubles. Here are some common things to think about:

| Source of Financial Problem | Reason Why Difficulties Often Occur | Solution |

| Unemployment or lower than usual income | Using credit for living expenses on reduced income | Re-evaluate your lifestyle, create a budget and follow it. If employed, see if you can get a 2nd job or more overtime |

| Unexpected illness or accident | Increased medical expenses and low/no income | Simplify your lifestyle. Get all the help you can. Make sure you’re getting everything you’re entitled to: check with your province & reach out to agencies that can help |

| Moving out on your own | Used to a high standard of living that took your parents decades to achieve | Adjust expectations and learn to live on what you earn rather than what you’re used to; use cash, not credit |

| First baby is born | Parents didn’t budget for the increased expenses and the drop in income during maternity leave | Adjust your budget and your lifestyle to fit the reduced income and increased expenses |

| Divorce | Got the house but can’t afford the ongoing expenses on only one income; left over bills | Got the house but can’t afford the ongoing expenses on only one income; leftover bills |

| Retirement | You’re now asset rich and cash poor. You can no longer afford to live life plus pay the house upkeep on your reduced income | Sell the house, move into something you can afford, invest extra proceeds from the sale, and enjoy life more |

| Emotional attachment to something | You are not willing to part with something you can no longer afford: could be a home, business, vehicle or toy | Set emotions aside and look at the situation from a financial perspective; picture life 5 years from now & what bills will be then |

| An addiction | Set emotions aside and look at the situation from a financial perspective; picture life 5 years from now & what the bills will be then | Get professional help and counseling to deal with the addiction. If you don’t, you’ll never overcome your financial problems |

Your problem may not be listed above or it may be more complex. However, the concept of identifying a specific problem is important because it is more likely to result in a lasting solution. Just like with a leaky faucet; placing a bucket below is temporary. Fix the tap and the leak will stop. Focus on solving the problem that’s causing your money troubles, rather than dwelling on your stress.

2. Find ways to earn more money

You can only cut a budget so far, and you’ll want to be careful that your tight budget doesn’t become a source of additional stress. With the price of consumer goods being higher than normal, line items in your budget are likely already under strain.

It might be worth looking for ways to increase your income instead. Some ways to do so include:

- Work a few extra hours: Try talking to your employer about putting in some extra time each week, if you’re paid hourly or at least eligible for overtime pay.

- Negotiating for a raise: Given high inflation and a tight labor market, employers may be more willing to grant a pay increase.

- Selling items you no longer need: This can include things such as old furniture, clothing, toys, pet items and tools.

- Taking on a side gig: A side gig can be a good option for those who want a flexible way to pad their income alongside a full-time job. This can include things like delivering food, tutoring or running a blog. The money can really add up, considering the monthly average and median income from side hustles in 2022 was $996 and $400, respectively, according to a Bankrate survey.

3. Create a Budget – Spend Money in a Way That Helps Solve the Problem

One of the best weapons for combating financial problems is a budget. A budget is a monthly spending plan for your money. Creating a budget is like turning the lights on to find your way around a dark room. You no longer need to wander in the dark; banging your shins, tripping over the furniture, and stepping on the dog.

Instead, with the lights on, you can see what’s going on and prevent problems before they happen. A budget works much the same way; it guides your spending decisions so that you’re spending money on what’s really important to you. In this case, you’ll spend your money in a way that helps solve your financial problem.

Track Your Expenses to Build a Budget That Works

As you create your budget, it’s important that your expenses aren’t just guesses – they need to reflect reality. You may want to track your expenses for at least a couple of weeks (a month is best) to objectively see where you are spending your money and how much you’re spending. Although you may think you know where your money is going, when most people tally up all their purchases for a month, they are usually quite surprised to notice that their spending doesn’t always match up with what they thought their priorities were.

Once you’re confident the numbers in your budget are realistic, you can look at your budget critically and search for areas where you can save money. You’ll want to ask yourself things like: Do I need to eat out this much? Do I need to spend on entertainment or hobbies this month? Could I pack a lunch for work rather than buy one?” Asking yourself these questions doesn’t mean you’re cheap or restricted by your budget. It means that you’ve got bigger things to accomplish or worry about, things that can be solved by making some small changes.

4. Identify Small Steps You Can Take to Address the Problem and achieve Your Goals

The solution to financial problems is often to reduce expenses, increase income, or do some combination of both. This might not be something you want to do, and you’re not alone. Most people don’t want to make changes to their lifestyle, but faced with the choice of ongoing money troubles, or making several small changes to ease up on the financial stress – most people are game to try.

Big changes are always much harder than small changes so to accomplish your goals, identify small steps you can take to achieve them. If you keep running into money problems because you’re $50 short every month, then maybe one of your first short-term goals could be to pay off a small credit card balance that requires a $50 minimum payment each month.

However, if by the time you reach this goal, you’ve learned to get by without this $50, then use it to accelerate the payment of another debt each month, and get all of your debts paid off more quickly.

There is actually a name for this, it is called the “snowball effect” – maintaining minimum payments on all debts but putting all extra money towards one debt to get it paid off faster. Once that one debt is paid off, you put all of the extra funds toward eliminating the next debt. It’s one powerful method of paying debts off faster.

- Look for Things You Can Do, Even Temporarily, to Improve Your Situation

Here are more ideas or steps you can consider taking to improve your financial situation and alleviate difficulties:

- As you look through your budget, ask yourself: Do I want this or do I need it? Will spending this money get me closer to my financial goals or further away? Can I live without it?

- Do you use credit cards for impulse purchases? This can contribute to a cycle of ongoing financial difficulty and add as much as 50% to everything you purchase.

- Ask yourself if you can downsize anything in your budget or switch to a less expensive option. If vehicle costs are straining your budget, can you downsize your vehicle, get rid of one vehicle (the average person spends over $9,000 per year to own and operate a vehicle), take transit (80% cheaper than owning a vehicle), or carpool? If your rent, mortgage, or home upkeep is bleeding you dry, can you downsize to something more affordable, rent out your basement, rent a room in your house, rent out the storage space in your garage, or can you take in a student for some extra income?

- Can you take on a side job or create another source of income with something you know how to do well?

- Look outside the box, ask yourself tough questions, invite a trusted friend to have a look at your budget and make suggestions, or sit down with a Credit Counsellor and get their suggestions.

- Research viable options that will move you toward your goals. A consolidation loan, speaking with a Credit Counsellor, a Debt Management Program, or some other option may be a possibility.

While doing any of these can be an unappealing thought, don’t just dismiss them because they’ll move you out of your comfort zone. Keep thinking about them and give them some consideration. Come back to these ideas from time to time to see if you can come up with a new angle on decreasing your expenses or increasing your income that might just work for you. Remember, you’re trying to get through a tough time; you don’t need to do this forever, just to get back on track. If you’re really struggling, an experienced Credit Counsellor can be a great, free source of suggestions.

5. Develop Your Plan to Overcome Financial Problems for Good

Once you’ve come up with some ideas for how to begin tackling your financial problems and difficulties, you can put together a realistic plan to accomplish your goals. Some goals will have a timeline of a few months; others will need a longer timeline, like 24 – 36 months. Write your goals down, but also write down where you’re at now in relation to each goal.

For example, if one of your goals is to pay off a $4,000 debt, make sure to write down the current debt balance and your future goal of paying this down to $0. You’ll want to include in your plan the amount of money you’re going to pay on this debt every month so that you can pay it off within your desired time frame.

If you’re really feeling overwhelmed and stressed by your situation, you can also reach out to a non-profit credit counselling agency for help. They have professionally trained Credit & Debt Counsellors who can review your situation with you, help you put together a realistic budget, and help you come up with a plan to solve your current challenges and get your finances back on track. Their help is usually free and is always confidential.

6. Review How Things are Going

The last step takes place once you are a few months into working on your plan. Every once-in-a-while, take a few minutes to review how things are going. Is your plan working? Are you making progress toward your goals? If not, you’ll need to take a closer look to figure out why not and adjust your plan. Your plan needs to be realistic, or it’s not going to work. It should also contain some things you weren’t doing before you put the plan in place.

If you keep doing what you were doing before, then you’ll continue to get the same result as before – problems. You’ve got to do something different to get a different outcome.

As you follow your plan and see improvements in your situation, be open to the possibility of fine-tuning the plan. Once you start making some progress, you may find you’re doing better than you thought, or you may come up with some new insights. Improving your plan so that you accomplish your goals more quickly is good as long as your budget can afford the changes and everyone who relies on your budget is okay with the more aggressive approach.

7. Consult with an expert financial advisor

Consider talking to a financial advisor to help take some of the weight off your shoulders when it comes to things like setting goals, saving money and decreasing debt. Working with a financial advisor on aspects that include financial planning and investment selection can add around 3 percent to your portfolio annually, based on research by consulting group Envestnet | PMC.

“In times of stress, a financial advisor should be there to validate your feelings [and also] show you why you should feel calm with the plan you have in place,” says Money Habitudes’ Macksoud. “If you have a longer-term relationship with an advisor, the greatest part of that is you can see where you were, where you are, and where you’re going. And if you’re still on track, even with market uncertainty as it is, you should find peace with the diversification you have.”

Navigating Social Influences and Peer Pressure

Social influence plays a significant role in shaping our purchasing decisions. Whether it’s through recommendations from friends, online reviews, or the influence of celebrities, we are constantly being influenced by others when making purchasing choices.

The influence of Social media

Social media platforms have revolutionized the way we interact with brands and make purchasing decisions. Influencers, who have amassed a large following on platforms like Instagram or YouTube, hold significant sway over their audiences. When an influencer promotes a product or service, their followers often perceive it as a personal recommendation and are more likely to try it themselves. For example, a beauty influencer showcasing a new makeup brand’s products and demonstrating their effectiveness can prompt their followers to purchase those items.

A notable case study illustrating the impact of social influence on purchasing is Coca-Cola’s “Share a Coke” campaign. In 2011, Coca-Cola replaced its iconic logo on bottles and cans with popular names and phrases. The campaign aimed to encourage consumers to purchase Coca-Cola products and share them with others, leveraging the power of personalization and social influence. By seeing bottles with their names or those of their friends, consumers felt a sense of connection and were more likely to buy and share the product, leading to increased sales for Coca-Cola.

Navigating Financial Discussions With Friends and Family

Friends and family play a significant role in shaping our preferences and influencing our purchase decisions. Whether we realize it or not, their opinions, recommendations, and experiences can greatly impact the products and brands we choose.

- 1. Word-of-Mouth Recommendations:

One of the most common ways in which friends and family influence our purchase decisions is through word-of-mouth recommendations. When someone we trust recommends a product or service, we are more likely to consider it seriously. For example, imagine you are contemplating buying a new smartphone. If your best friend raves about the features and performance of a particular brand, you are more likely to give it a try based on their positive experience.

- 2. Social Proof:

Humans have a natural tendency to conform and seek validation from others. This phenomenon, known as social proof, can heavily influence our purchasing choices. When we see our friends or family members using a certain product or brand, we may feel compelled to follow suit to fit in or be part of the trend. For instance, if everyone in your social circle starts using a specific fitness tracker, you might feel inclined to join them to feel socially connected and avoid missing out.

- 3. Emotional Connection:

Friends and family have a deep understanding of our likes, dislikes, and aspirations. They are aware of our personal preferences, lifestyle choices, and values. As a result, their recommendations can resonate with us on an emotional level. Suppose you are considering purchasing a new car, and your sibling suggests a hybrid model that aligns with your eco-friendly values. Their recommendation may carry more weight due to the emotional connection and shared values you have with them.

- 4. Social Media influence:

In today’s digital age, social media has become a powerful platform for friends and family to influence our purchase decisions. Platforms like Instagram, Facebook, and YouTube are filled with product recommendations, reviews, and endorsements from our social circle. Influencers, who are often friends or acquaintances, can sway our opinions through their posts and stories. For example, if a close friend posts about a new skincare product they love, it may pique your interest and lead you to explore it further.

- 5. Case Study: The impact of Online reviews:

Online reviews, often shared by people we don’t know personally, can also influence our purchase decisions indirectly. However, these reviews can be seen as a form of social influence since they reflect the experiences and opinions of other consumers. Research has shown that positive reviews from strangers can be as persuasive as personal recommendations from friends and family. Therefore, when we come across a product with numerous positive reviews, we are more likely to trust it and feel confident in making the purchase.

Tips for Navigating Social Influence:

– Be aware of the influence friends and family have on your purchase decisions and take a moment to evaluate if their recommendations align with your needs and preferences.

– Seek a variety of opinions and do your own research before making a purchase to ensure you are making an informed decision.

– Consider your own values and priorities when evaluating the recommendations of friends and family. What works for them may not necessarily work for you.

In conclusion, friends and family have a powerful influence on our purchase decisions. Their recommendations, social proof, emotional connections, and the impact of social media all contribute to shaping our preferences. By being mindful of the influence they hold, we can make more informed choices that align with our own needs and values.

Conclusion

There are a lot of variables in life. And it’s no different in the world of personal finance. A lot of things can happen with our money–we might make a bad investment or two, an unexpected emergency can wipe out our emergency fund, or we might even get lucky with an investment.

The one constant though is our attitude and the way we think about money. It’s the one thing we can control, no matter what happens. We have the ability to create a positive money mindset.

There are certain and intentional steps we all can take to greatly improve our mindset around money. These steps don’t have to be time-consuming either–a lot of it is simply being aware and making the necessary adjustments.

- Figure Out Your Why

A great starting point to improve your money mindset is to figure out your why. What is your why for improving your money mindset and attitude? Why do you want to improve in your personal finances?

Are you wanting to improve to change your family’s financial future? Do you want to take more vacations and have more control over your time? Or is it more about reaching your full potential, which includes financial success?

For many, it might be a combination of things. Figure out your why–there is no right or wrong answer here. A great starting point to improve your money mindset is to figure out your why. What is your why for improving your money mindset and attitude? Why do you want to improve in your personal finances?

Are you wanting to improve to change your family’s financial future? Do you want to take more vacations and have more control over your time? Or is it more about reaching your full potential, which includes financial success?

For many, it might be a combination of things. Figure out your why–there is no right or wrong answer here.

- Write Down What You’re Good At

This next step seems simple, and it can be. You just have set some time aside and get it done. Take about 20 minutes and write down what you are good at. It doesn’t matter how insignificant you might think it is–take some time and write it down.

Writing things down has a way of creating clarity and recognizing patterns. There’s also a magic to seeing things in writing–words have a way of popping off the page when you write them down. Some things to consider writing down:

- What are you good at that you enjoy?

- Describe your ideal day.

- What feels light to you and what feels heavy?

- What would you like to be doing 10 years from now?

- Think Abundance

Do you believe that money is an infinite resource you can make more of, or do you believe money is limited and scarce? Speaking for myself, I used to think of money as scarce and something that had to be stored away in hopes I wouldn’t lose it. I’ve since shifted to the abundance mindset.

The person with an abundance mindset looks for win-wins, new opportunities, and problems that need to be solved. They find opportunity in everything, even if it looks like a bad thing at first. Since inflation has been running rampant over the past several months, let’s use it as an example.

Inflation presents a lot of challenges and problems for people. Their spending power is reduced seemingly overnight. Gas that used to cost four dollars a gallon is five or six dollars a gallon. Produce that used to cost 99 cents/lb. now costs $1.35/lb. A person with an abundance mindset looks for ways to win during an inflationary period.

Maybe it’s changing an investment strategy to hedge against inflation. Or maybe a new business is started to help people overcome the challenges inflation presents. Whatever it is, the individual with an abundance mindset is looking for ways they can win and help others during this time period.

- Get Educated

One of the best ways to begin shifting your money mindset is to get educated. Education helped me shift from excuse-ridden and financially unsuccessful to someone who takes accountability and ownership for my personal finances. The missing piece was education.

Book Recommendations:

- Rich Dad Poor Dad

- The Millionaire Next Door

- Set for Life

- The Richest Man in Babylon

- The Automatic Millionaire

- Change Your Habits

This is where it’s all about taking action. Changing your habits is one of the best ways to take action. It’s easy to sit around and think about things and ruminate about things that never will happen. But when we take action, we don’t have to sit around and worry because we are too busy doing.

Habits are formed as we begin doing and implementing. For example, if your job requires you to make contact with 10-15 customers per day to succeed, that’s an essential action. Once you begin making those 10-15 contacts per day, it will start to become a habit.

The idea is after making the client contacts for a set amount of time, it will become second nature and a habit. Rather than worrying about losing customers, you will be taking action to strengthen client relationships and build a greater client base.

- Take Action

Piggybacking off changing habits is taking action. Taking action means getting things done. Making mistakes, picking yourself up, and moving along. Some of our actions are going to work and some aren’t.

The ones that work may become habits, the ones that don’t work get tossed out and replaced with actions that work. When we take action, we change our mindsets into the “doer mindset.” The doer gets things done and doesn’t dwell on the things that didn’t work.

Taking action also helps to build a mindset of confidence. Confidence to know that mistakes will be made and obstacles overcome. When people acquire this mindset, they are not as afraid to take action and make mistakes. Eventually past failures turn into future successes–all part of the growth process.

It’s not hard to create a more positive money mindset. It’s also not easy. You have to make the choice that you want to improve it. If you make the choice to improve your money mindset, then you will. If you make the choice not to, you won’t.

Once you do make the choice though, it’s simply a matter of taking action and being consistent. The results will come. Some results will come faster than expected, other results will come slower. It’s all about making progress though, and getting better every day.