The qualified business income deduction (QBI) is a tax deduction that allows eligible self-employed and small-business owners to deduct up to 20% of their qualified business income on their taxes.

In general, total taxable income in 2020 must be under $163,300 for single filers or $326,600 for joint filers to qualify. In 2021, the limits rise to $164,900 for single filers and $329,800 for joint filers.

If you’re over that limit, complicated IRS rules determine whether your business income qualifies for a full or partial deduction. This article will tell you all you need to know about qualified business income deductions.

- Who Qualifies For Qualified Business Deductions?

- What is Included in Qualified Business Income?

- How is Qualified Business Income Deduction Calculated?

- What Business Does Not Qualify For QBI Deduction?

- QBI Deduction Calculator

- Qualified Business Income Deduction Worksheet

- What is a Qualified Trade or Business?

- Qualified Business Income Deduction Rental Property

- Section 199A Examples

- Qualified Business Income Deduction Turbo Tax

- QBI Deduction Limitation

- Qualified Business Income Deduction Simplified Computation

- Qualified Trade or Business Under Section 199A

Who Qualifies For Qualified Business Deductions?

The qualified business income deduction is for people who have “pass-through income” — that’s business income that you report on your personal tax return.

Entities eligible for the qualified business income deduction include:

- Sole proprietorship

- Partnerships.

- S corporations.

- Limited liability companies (LLCs).

The qualified business income deduction by definition applies to “qualified business income,” or QBI. Qualified business income is defined as “the net amount of qualified items of income, gain, deduction and loss with respect to any trade or business.” Broadly speaking, that means your business’s net profit.

Read Also: How to Trademark a Business Name

But it also means that not all business income qualifies. QBI excludes:

- Capital gains or losses.

- Dividends.

- Interest income.

- Income earned outside the U.S.

- Certain wage and guaranteed payments made to partners and shareholders.

What is Included in Qualified Business Income?

QBI doesn’t include any of the following.

- Items not properly includible in income, such as losses or deductions disallowed under the basis, at-risk, passive loss or excess business loss rules.

- Investment items such as capital gains or losses, or dividends.

- Interest income not properly allocable to a trade or business.

- Wage income.

- Income not effectively connected with the conduct of business within the U.S. (For more information, go to IRS.gov/eci).

- Commodities transactions or foreign currency gains or losses.

- Income, loss, or deductions from notional principal contracts.

- Annuities (unless received in connection with the trade or business).

- Amounts received as reasonable compensation from an S corporation.

- Amounts received as guaranteed payments from a partnership.

- Payments received by a partner for services other than in a capacity as a partner.

- Qualified REIT dividends.

- Qualified PTP income.

How is Qualified Business Income Deduction Calculated?

Start by using your taxable income, NOT your adjusted gross income (AGI). Your taxable income is your gross income after you’ve subtracted your deductions and personal exemptions.

Remember to determine your QBI separately for each of your qualified businesses, then combine them all as a single amount on your tax return.

Step 1. Determine whether your income is related to a qualified trade or business

You must have an ownership interest in a qualified trade or business to claim the QBI deduction. A qualified business is a partnership, S corporation, or sole proprietorship. They’re also known as pass-through entities.

However, some businesses might face a limited deduction. They’re called specified service trades or businesses or SSTBs.

SSTBs include businesses in the following industries: health, law, accounting, actuarial science, performing arts, consulting, athletics, investing and investment management, and trading. SSTBs also include any business with a principal asset of a reputation or skill of one or more of its employees or owners and businesses dealing in securities, partnership interests, or commodities.

If your business falls under any of these categories, there’s a chance you can’t claim this deduction. If you can claim it, your deduction amount might be limited.

Step 2. Calculate the QBI for each business for the tax year and your net taxable income.

QBI is the net amount of the business’ qualified items of income, gain, deduction, and loss. It doesn’t include investment-related items of income, gain, deduction, and loss. These rules also apply to active and passive investments.

What’s not QBI?

- Amounts paid for services that are your reasonable compensation*

- Guaranteed payments to a taxpayer for services performed

- Amounts paid to a taxpayer that’s acting outside of his/her capacity as a partner for services

- Qualified REIT dividends

- Qualified cooperative dividends

- Income from foreign pass-through entities

- Qualified PTP income

Usually, you can deduct 20% of qualified REIT dividends, qualified cooperative dividends, and qualified PTP income, but you don’t include these items when calculating your QBI.

*Reasonable compensation is limited to the compensation of S corporation shareholders-employees. It doesn’t apply to partnerships.

Can I combine QBI sources?

Yes. In order to calculate your total QBI, you can combine multiple sources of income. If you have two or more businesses, you can combine the QBI, W-2 wages, and basis of qualified property for each of them. Then, you apply the W-2 wage and qualified property limitations. You aren’t required to combine – or aggregate – your businesses, but it’s allowed.

If you do choose to aggregate, your businesses have to meet certain criteria and requirements. And, you would have to continue to aggregate in future years until circumstances change.

Now that you’ve calculated your QBI for each of your businesses, let’s move on to calculating your limitation. Unfortunately, you may not always get to claim a straightforward 20% deduction. It may be limited.

Calculating your limitation will help you decide if aggregating your businesses hurts or helps your total deduction amount.

Step 3. Apply the W-2 wages and qualified property limitation

You must calculate your limitation if:

- You have ownership interest in a qualified trade or business

AND

- Your 2020 taxable income is more than $326,600 as a married filing jointly taxpayer or more than $163,300 as a single taxpayer

If your taxable income is less than these amounts, you don’t have to calculate the limitation. You can take the straight 20% deduction.

To calculate your limitation, you need to know how much the company paid in W-2 wages and how much qualified property it has. W-2 wages are the total W-2 wages the company paid to employees that are subject to tax withholding, elective deferrals, and deferred compensation. Qualified property is tangible property – personal or real – that’s subject to depreciation. The land isn’t qualified property.

Then, you’ll have to do some math. Your QBI is limited to whichever of the following options is the lowest:

- 20% of your QBI

OR

- 50% of the company’s W-2 wages OR the sum of 25% of the W-2 wages plus 2.5% of the unadjusted basis of all qualified property. You can choose whichever of these two wage tests gives you a greater deduction.

Step 4. This is your total deduction amount

You’ve successfully calculated your deduction amount! If the net amount of your combined QBI during the tax year is a loss, you carry the loss forward into the next tax year.

Let’s look at an example.

Mary is married. Her filing status is married filing jointly. She owns a manufacturing business that generates $100,000 of QBI. Her taxable income is more than $415,000. The business paid $30,000 in wages and has $50,000 in qualified property.

Because Mary’s taxable income is more than $326,600, she can’t automatically claim the 20% deduction. She has to calculate her limitation. She performs both wage tests to find the greatest deduction.

Test 1: 50% of the company’s W-2 wages

50% x $30,000 = $15,000

Test 2: 25% of the W-2 wages plus 2.5% of the unadjusted basis of all qualified property

(25% x $30,000) + (2.5% x $50,000) = $8,750

Mary chooses the greater deduction, so her total QBI deduction amount is $15,000.

Now, if Mary’s taxable income was less than $326,600, her QBI deduction would have been $20,000 (20% x $100,000).

We know this deduction can quickly become complicated with eligibility rules, definitions, aggregation requirements, and applying the wage tests. The good news is, tax professionals can help you figure out if you can claim this deduction and calculate your total deduction amount. You don’t want to miss out on a 20% tax deduction.

What Business Does Not Qualify For QBI Deduction?

Individuals, trusts, and estates with qualified business income (QBI) from a partnership, S corporation, or sole proprietorship may qualify for the QBI deduction. Any income you receive from a C corporation isn’t eligible for the deduction.

Some factors such as income limits and the type of business you run may affect your eligibility.

Unfortunately, if your 2021 taxable income is greater than $429,800 (MFJ) or $214,900 (other) and your business is a specified service trade or business, you can’t claim this deduction. At all.

What’s a specified service trade or business (SSTB)? Businesses that fall within the following industries:

- Health

- Law

- Accounting

- Actuarial science

- Performing arts

- Consulting

- Athletics

- Investing & investment management

- Trading

- Dealing in securities, partnership interests, or commodities

- Any business with a principal asset of a reputation or skill of one or more of its employees or owners

If you don’t know whether your business is a SSTB, the IRS regulations state, “In many cases, the determination of whether a specific trade or business is an SSTB depends on whether the facts and circumstances demonstrate that the trade or business is in one of the listed fields,” (TD-REG-107892-18).

Essentially, each business is unique. The IRS doesn’t have clear-cut rules on which businesses fall within these categories. You and your tax professional will need to analyze your business, determine the services it provides, and decide whether it’s a specified service trade or business.

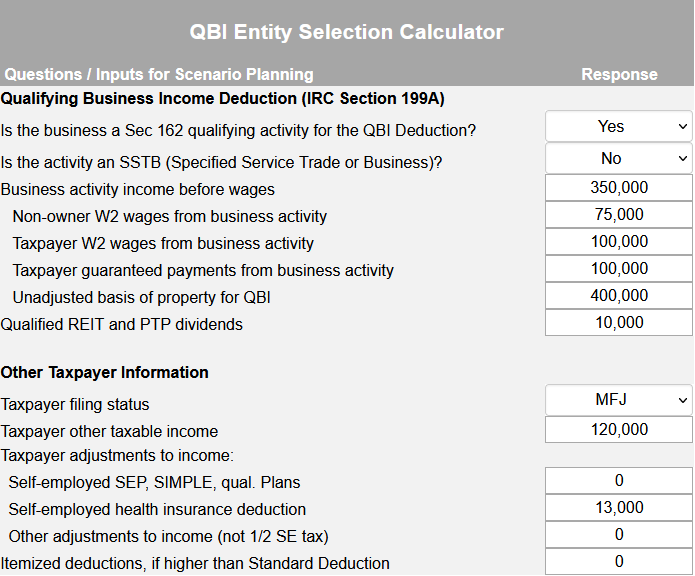

QBI Deduction Calculator

This worksheet is designed for Tax Professionals to evaluate the type of legal entity a business should consider, including the application of the Qualified Business Income (QBI) deduction. The best tax strategies may include a combination of business entities to optimize the tax results for the taxpayer. Below is an example.

Qualified Business Income Deduction Worksheet

| Line | QBI Entity Selection Calculator | Schedule C/F | Schedule E Rental | Partnership K-1 | S Corp K-1 | C Corp | |

| 1 | |||||||

| Non-owner W2 wages | |||||||

| Taxpayer W2 wages | $0 | $0 | $0 | ||||

| Guaranteed payments | $0 | $0 | $0 | $0 | |||

| Net income from business activity for QBI deduction | |||||||

| Federal Individual Tax Return Summary | |||||||

| W2 wages / Guaranteed payments | $0 | $0 | |||||

| Qualified REIT and PTP dividends | |||||||

| Less: Adjustments to income | |||||||

| Less: Standard or itemized deductions | |||||||

| Taxable income before QBI | |||||||

| Less: QBI Deduction | |||||||

| Taxable Income | |||||||

| SE Tax / Payroll Taxes on owner’s wages | |||||||

| Federal Individual Income Tax | |||||||

| Corporate Tax (21%) | NA | NA | NA | NA | |||

| Total Taxes | |||||||

| Net Cash to Owner (Salary, K-1, -Taxes) | |||||||

| C Corp Cash Retained | |||||||

| Total Cash After Taxes | |||||||

DISCLAIMER: This worksheet is one tool in the consideration process and should not be relied upon without the advice of a professional who understands all the facts and relevant implications.

This worksheet provides directional analysis and will not predict actual results. Additional considerations not included in this analysis, such as State Taxes, should be evaluated for entity selection considerations

What is a Qualified Trade or Business?

A qualified trade or business is any trade or business except one involving the performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, investing and investment management, trading, dealing in certain assets or any trade or business where the principal asset is the reputation or skill of one or more of its employees.

This exclusion only applies, however, if a taxpayer’s taxable income exceeds $315,000 for a married couple filing a joint return, or $157,500 for all other taxpayers.

While relatively straightforward for most businesses, those with more complicated tax structures or multiple businesses or trades, consulting a tax professional is advised.

Qualified Business Income Deduction Rental Property

Most rental real estate owners have heard about the new qualified business income deduction (QBI deduction), and many are asking, “Do I qualify for the QBI deduction?” Anytime a new federal tax law changes the rules for small businesses, these taxpayers must determine whether the changes apply to rental real property owners. The answer is far from clear and involves interpretation of many sources of law including the Code, IRS guidance, and case law.

The Tax Cuts and Jobs Act of 2017 (TCJA) created the qualified business income deduction, a new deduction that most business owners can take in tax years 2018 through 2025.

Generally, the deduction is equal to the lesser of 20 percent of qualified business income or 20 percent of taxable income less net capital gain. Qualified business income is the net income from a qualifying business minus certain items such as capital gains.

There are many limitations and special rules that may apply when determining if a taxpayer qualifies for the qualified business income deduction. The first rule is that the taxpayer must have business income from either a sole proprietorship, an LLC taxed as a disregarded entity, a partnership, or an S corporation.

These entities are unique in that they are not taxed at the entity level, rather, items of income, gain, loss, and expense flow through to and are reported on the owners’ individual returns. This means the QBI deduction is claimed on the individual owner’s return.

Section 199A Examples

Below are examples and commentary addressing Section 199A.

Side Hustler

Mike works a full-time job. His W-2 for 2018 reports $90,000 of wages. Mike also receives $1,000 of qualified dividend income (“QDI”) in his taxable account. Mike has a side hustle where he nets $10,000 in Schedule C profit. Mike pays $1,413 in self-employment tax on that profit. Mike claims the standard deduction.

Recall that the Section 199A deduction is the lesser of:

- 20 percent of your taxable income less your “net capital gain” which is generally your capital gains plus your QDI; or,

- 20 percent of your qualified business income (“QBI”).

The deduction for one-half of self-employment taxes is factored into the determination of QBI. Thus, in Mike’s case, his Section 199A deduction is the lesser of:

- 20% of Taxable Income: 20% times ($90,000 plus $10,000 plus $1,000 less $707 less $1,000 less $12,000 = $87,293) = $17,459; or,

- 20% of QBI: 20% times ($10,000 less $707 = $9,293) = $1,859

In this case, Mike’s Section 199A deduction is $1,859.

Mike’s taxable income is determined by deducting, for adjusted gross income, one-half of the self-employment taxes ($707) he pays with respect to his side hustle income. However, that deduction for half of his self-employment tax must also be subtracted in determining his QBI.

Note further that the Section 199A deduction does not reduce self-employment taxes. The Section 199A deduction is only an income tax deduction. It does not reduce the amount subject to self-employment taxes (in Mike’s case, $10,000).

Sole Proprietor with a Solo 401(k)

Lisa owns a sole-proprietorship that generates $100,000 of business income in 2020 as reported on Schedule C. Lisa pays $14,130 in self-employment taxes. Lisa contributed $19,500 to her traditional Solo 401(k), and makes an employer contribution to her traditional Solo 401(k) of $18,587. Lisa is married to Joe who makes $75,000 in W-2 wages. Lisa and Joe claim the standard deduction.

The deduction for retirement plan contributions is factored into the determination of QBI. Thus, in Lisa’s case, her Section 199A deduction is the lesser of:

- 20% of Taxable Income: 20% times ($100,000 plus $75,000 less $7,065 less $19,500 less $18,587 less $24,800 = $105,048) = $21,010; or,

- 20% of QBI: 20% times ($100,000 less $7,065 less $19,500 less $18,587 = $54,848) = $10,970

In this case, Lisa’s Section 199A deduction is $10,970.

QBI has the effect of making certain income “80% income.” What I mean by that term is that only 80% of the income is subject to income tax. This has a flip side – some deductions become only “80% deductions,” meaning that only 80% of the deduction generates a tax break.

Notice that the Solo 401(k) contributions reduce the QBI deduction. Thus, Solo 401(k) contributions are now “80% deductions” due to the QBI regime. For example, if your marginal tax rate is 22 percent, the marginal tax rate savings on your traditional 401(k) employee contribution is only 17.6 percent. But years later, when you withdraw the money from the Solo 401(k) the money will be “100% income.” You will not get a QBI deduction for those withdrawals.

This will cause many sole proprietors to consider Roth Solo 401(k) employee contributions instead of traditional Solo 401(k) employee contributions since the tax savings on traditional self-employed employee contributions is reduced as a result of the QBI deduction.

Note further that for the Solo 401(k) employer contribution there is no choice to be made because there is no option to make a Roth employer contribution. All employer contributions must be traditional contributions.

Another observation: If Lisa and Joe had a low enough adjusted gross income (under $105,000) and Lisa made a deductible $6,000 contribution to a traditional IRA, that contribution would not have counted against her QBI. A contribution to a health savings account would also not have lowered her QBI.

For taxpayers whose Section 199A deduction is limited by 20% of QBI, contributions to traditional IRAs and HSAs should be favored over self-employment retirement plan contributions, since the IRA and HSA deductions are 100% deductions while the self-employment retirement plan contributions are 80% deductions. Hat tip to Jeff Levine who made the retirement plan contribution prioritization point on Twitter.

For taxpayers whose Section 199A deduction is limited by 20% of taxable income, contributions to traditional IRAs, HSAs, and self-employment retirement plans are all 80% deductions, and thus Section 199A normally does not factor into determining how to prioritize these contributions. However, all of these are tools taxpayers may be able to use to lower taxable income to qualify for a Section 199A deduction, as discussed in the Managing Taxable Income section below.

S Corporation

Assume the facts are the same as the previous example, except for the following differences. Lisa operates her business as a wholly-owned S corporation instead of as sole proprietorship. Before any sort of compensation, the S corporation makes $100,000. Assume that in this case, the S corporation pays Lisa $50,000 of W-2 wages, which is further assumed to be reasonable.

Lisa makes employee contributions of $19,500 to her traditional Solo 401(k) from those wages. The S corporation makes the maximum employer contribution of $12,500 (computed as $30,500 of Box 1 W-2 wages plus $19,500 of elective deferrals times 25 percent). Thus, Lisa will have flow-through income from the S corporation (reported to her on a Schedule K-1) of $33,675 ($50,000 less $12,500 less $3,825 — the employer portion of the payroll tax).

Thus, in Lisa’s case, her Section 199A deduction is the lesser of:

- 20% of Taxable Income: 20% times ($50,000 plus $33,675 plus $75,000 less $19,500 less $24,800 = $114,375) = $22,875; or,

- 20% of QBI: 20% times ($33,675 — the QBI) = $6,735

In this case, Lisa’s Section 199A deduction is $6,735 because in the S corporation structure, the business income is split between a salary the S corporation pays her (which is not QBI) and the flow through profit of the S corporation, which is QBI (assuming it is domestic trade or business income).

The S corporation has various pros and cons from a tax perspective. Lower employment (payroll) taxes are a significant benefit, while lower maximum employer retirement plan contributions and lower Section 199A deductions are drawbacks.

Managing Taxable Income

Jackie is a lawyer operating as a sole proprietor. Law is one of several specified service trade or businesses (“SSTBs”) where the benefits of Section 199A are completely phased out if your taxable income exceeds $213,300 ($426,600 for married filing joint taxpayers using 2020 numbers).

In 2020 Jackie has $240,000 of Schedule C income from the business. His self-employment taxes are $17,075 in Social Security taxes and $6,428 in Medicare taxes, for a total of $23,503 reported on Schedule SE. Jackie takes the standard deduction.

Jackie’s taxable income is thus $215,848 ($240,000 less $11,752 less $12,400). Because Jackie’s QBI is from an SSTB and his taxable income is above $213,300, he cannot claim any Section 199A deduction.

Now let’s add some tax planning to the scenario. Imagine that early in 2020 Jackie realizes he won’t qualify for the Section 199A deduction based on his numbers. He decides to open a Solo 401(k), which he can make an $19,500 employee traditional contribution to, and he can make an employer contribution of $37,500 for total contributions of $57,000 (the maximum allowed).

This radically changes his Section 199A math, since (as will be demonstrated) his taxable income is now below $163,300. Once your income is below $163,300, you qualify for the Section 199A deduction only subject to the computational limits. Thus, in Jackie’s case, his Section 199A deduction is the lesser of:

- 20% of Taxable Income: 20% times ($240,000 less $11,752 less $12,400 less $57,000 = $158,848) = $31,770; or,

- 20% of QBI: 20% times ($240,000 less $11,752 less $57,000 = $171,248) = $34,250

Thus, Jackie’s Section 199A deduction is now $31,770! By managing his taxable income (by maximizing retirement savings), Jackie turned a $57,000 deduction into a more than $88,000 of deductions. Sure, the $57,000 deduction for retirement plan contributions is an “80% deduction,” but it creates the additional $31,770 of a Section 199A deduction (which is itself a “100 percent” deduction).

Jackie also lowered his marginal federal income tax rate from 35 percent to 24 percent and reduced his taxable income from $215,848 to $127,078!

Note that contributions to a health savings account would be another tool to deploy to lower your taxable income if you are concerned about Section 199A’s taxable income limitations.

Taxpayers bumping up against Section 199A taxable income limitations will likely need to prioritize traditional employee contributions to Solo 401(k) plans over Roth employee contributions. In addition, self-employed taxpayers bumping up against the taxable income limits in 2021 may want to establish 2021 Solo 401(k)s (if they are eligible to do so) to lower taxable income in order to qualify for the Section 199A deduction.

It will be wise for taxpayers to consult with tax advisors to run the numbers on Section 199A and other tax planning considering the complexity of the rules and the potential benefits of successful planning.

Charitable Contributions

The IRS gave us a bit of a head-scratcher in the instructions to the new Form 8995. The Form 8995 is used (starting with 2019 tax returns) to compute the QBI deduction. In the instructions, it states that charitable contributions reduce QBI.

Here is an example of how that rule would play out:

Cosmo is the sole shareholder of Acme Industries, an S corporation. In 2019, Acme reports QBI operating income of $100,000 to Cosmo on his Form K-1. It also reports $1,000 of charitable contributions made by Acme during 2019. The total QBI Cosmo can claim from Acme Industries is only $99,000, as the charitable contribution reduces QBI, according to the IRS. This is true even if Cosmo claims the standard deduction and thus has no use for the charitable contribution on his 2019 tax return.

Personally, I believe the IRS is on the questionable ground in claiming charitable contributions reduce qualified business income. However, with some rather simple tax planning (which I generally believe to be prudent), you can avoid this issue altogether.

If you want to make a charitable contribution, simply do so in your own name. Do not have your business — whether an S corporation, a small partnership, or a sole proprietorship, make the charitable contribution.

Qualified Business Income Deduction Turbo Tax

At higher income levels, the deduction is reduced or eliminated, depending on the nature of the business. The calculations also get quite complicated, but TurboTax easily handles them and will figure out how much of a deduction you’re entitled to.

Don’t worry about memorizing these tax changes the majority of which are for 2018 taxes that you file in 2019. TurboTax has you covered and will be up to date with the latest tax laws.

TurboTax Live offers real tax experts and CPAs to help with your taxes—or even do them for you. You can get a final review of your tax return before you file to ensure your taxes are done right, or you can even have a dedicated tax expert do your taxes for you, from start to finish, with TurboTax Live Full Service.

You get unlimited tax advice year-round year, so you can be 100% confident your return is done right, guaranteed. TurboTax Live experts are highly knowledgeable, with an average 12 years of experience in professional tax preparation. Their tax advice, final reviews, and filed returns are guaranteed 100% accuracy.

QBI Deduction Limitation

If your total taxable income — that is, not just your business income but other income as well — is at or below $163,300 for single filers or $326,600 for joint filers, then in 2020 you may qualify for the 20% deduction on your taxable business income. In 2021, the limits rise to $164,900 for single filers and $329,800 for joint filers.

But if your income is above these limits, now’s the time to reach for a bottle of aspirin.

Here’s why: Above those income limits, your ability to claim the pass-through deduction depends on the precise nature of your business. And even if your business qualifies, there’s a chance you won’t get to enjoy the full 20% tax break, as the qualified business income deduction is phased out for some businesses.

Qualified Business Income Deduction Simplified Computation

For years beginning in 2019, the QBI deduction is calculated on one of two forms:

Form 8995 is the simplified computation form. You can use this form if your taxable income is not greater than $160,700 for an individual, $160,725 if married filing separately or married nonresident alien, or $321,400 if married filing jointly. (These amounts are for 2019 tax returns; the limits change each year.)

Form 8995-A is for more complicated situations, including SSTBs and multiple businesses.

S corporation owners and partners (including members of an LLC with multiple owners) calculate the QBI deduction differently. First, the total QBI for the business is calculated on one of the forms above.

Then each owner’s share of the QBI is calculated and entered in a separate line on the owner’s Schedule K-1, along with other income of the owner. Then the information on the Schedule K-1 is entered with the owner’s other income on the owner’s personal tax return.

Qualified Trade or Business Under Section 199A

Section 199A is a qualified business income (QBI) deduction. With this deduction, selecting types of domestic businesses can deduct roughly 20% of their QBI, along with 20% of their publicly traded partnership income (PTP) and real estate investment trust (REIT) income. The deduction is limited to 20% of taxable income, less net capital gains. Net capital gains refers to (capital gains less capital losses).

Read Also: How to Market Your Business

But, this deduction isn’t for everyone. There are income limitations as well as business limitations. First off, you need to file a joint return with no more than $315,000 in taxable income or a single return with a cap of $157,500 in taxable income for the tax year.

According to the IRS provision for Section 199A, the deduction is gradually phased out for joint return taxable income between $315,000 and $415,000. For other filers, the deduction is phased out for returns with taxable income between $157,500 and $207,500.

Businesses must also be domestic, meaning located within and taxed by the United States. And, businesses must be a sole proprietorship, partnership, S corporation, trust or estate to qualify.

There’s no getting around the fact that Section 199A is complicated. But, like all things tax-related, it’s much more manageable if you take your time and check every available tax resource. It’s especially manageable if you have a tax professional at your side. (They do this stuff for a living, after all.)

For the right small businesses, Section 199A can be a hearty deduction that lowers your taxable income by a substantial amount. For everyone else, it’s just a bunch of confusing tax jargon. In either event, speak to your tax or financial advisor, and see if this deduction is for you.