One of the oldest and largest financial institutions in the U.S., Citizens Bank offers a variety of bank products, including personal loans. Those products and the rest of the lending side of the company is branded as Citizens One.

The company’s personal loan rates can be competitive for those who have good to excellent credit. Those applicants may be able to borrow up to $50,000.

This Citizens Bank personal loan review dives into the details, to help you decide if this lender is a good fit for your financial needs.

- Is Citizens Bank Good For Personal Loans?

- What Credit Score do I Need to Get a Loan From Citizens Bank?

- Which Bank Personal Loan is Best?

- Is Citizens Bank Any Good?

- Citizens Bank Personal Loan Calculator

- Citizens Bank Student Loan Reviews

- Citizens Bank Student Loan

- What Credit Bureau Does Citizens Bank Pull?

- How do I Increase my Credit Limit With Citizens Bank?

- Does Citizens Bank Have a Credit Card?

- How Much Can I Withdrawal From ATM Citizens Bank?

- How do I Redeem my Citizens Bank Reward Points?

Is Citizens Bank Good For Personal Loans?

For existing Citizens Bank customers with good credit, Citizens Bank can be a great option for a personal loan. The bank offers unsecured personal loans from $5,000 to $50,000 with fixed or variable interest rates, with rates starting at 6.8%.

Citizens Banks looks for borrowers with good credit history and annual incomes of at least $24,000. One downside to Citizens Bank is that its personal loans cannot be used for home improvement, educational or business purposes.

Read Also: Best Egg Personal Loans Review

Citizens Bank is not a good choice for borrowers with average or lower credit scores. The bank looks for borrowers with strong credit history, which means a few or more years of credit history and a credit score of at least 680. The bank also requires borrowers to have a minimum annual income of $24,000.

However, these stricter eligibility requirements do translate into better rates and terms. APRs at Citizens Bank typically range from 6.8% to 20.91%, and borrowers have the option of getting a fixed or variable interest rate. Borrowers can also choose between three and seven years for their loan maturity.

Personal loans from Citizens Bank come with restrictions on their use, so if you’re planning on remodeling your home, paying for postsecondary educational expenses or starting a business, you’ll need to look elsewhere for a personal loan.

Currently, you can only use a Citizens Bank personal loan for debt consolidation, vacation or wedding expenses, major purchases, special occasions or adoption. However, Citizens Bank is available to residents in all states and Puerto Rico.

What Credit Score do I Need to Get a Loan From Citizens Bank?

The credit score thresholds change periodically, so the most convenient way to see if you qualify would be to a lending expert by phone, please contact our Mortgage Loan Customer Service at 1-888-514-2300. We are available from 8AM-8PM Monday-Friday.

We would suggest visiting our website at Citizens Bank Home Mortgages where you will find step by step details to help you get started. Here’s an overview of the process. We look forward to helping you along the way!

- Get Started – Figure out how much you can put down on a home, plus what mortgage payment fits your budget.

- Prequalify for Your Loan – Knowing how much you can borrow helps you proceed with confidence.

- Find the Right Fit – Match your dream home with the right home loan.

- Make an Offer – You’ve found the one. Now it’s time to place your offer. Then, you wait.

- Close Your Loan – You got the house! Review your documents, finalize the details, then celebrate!

Which Bank Personal Loan is Best?

1. SoFi

Overview: SoFi, a digital lender, offers products ranging from personal loans to student loan refinancing, private student loans, home loans, investing and various types of insurance. It’s working on becoming an all-encompassing place to save, spend and manage your money.

Personal loans, which are fee-free, range from $5,000 to $100,000 and must be repaid in two to seven years. Fixed-rate loans range from 5.99 percent APR to 18.85 percent APR.

Why SoFi is the best overall personal loan: SoFi offers a wide range of benefits that go beyond just funding your personal loan, including an autopay discount and unemployment protection in case you lose your job and need to pause payments on your loan.

Perks: SoFi offers career counseling and a referral bonus if a qualifying friend signs up. Members get personalized financial planning and aren’t charged any fees.

What to watch out for: You’ll need to have a solid credit score — at least 680 — to qualify for a SoFi loan.

2. LightStream

Overview: LightStream, a division of Truist, offers loans for practically any occasion, such as medical needs, pre-K-12 education or a family need.

Why LightStream is the best personal loan for generous repayment terms: Its loan terms range from two to seven years for most loans (and up to 12 years for loans for home improvement, swimming pools and solar energy systems), which means you can take longer to pay off your loan and benefit from lower monthly payments.

Perks: Loan amounts go up to $100,000, which is good if you have significant expenses. There are no fees and no prepayment penalties, and you get a 0.5 percentage point discount on your interest rate when you sign up for autopay.

What to watch out for: You’ll need to prove that you have a few years’ worth of credit history with many different account types to qualify. Delinquencies, defaults and late payments could hurt your eligibility chances

3. Avant

Overview: Avant offers loans as low as $2,000, which is helpful if you don’t need to borrow a lot of money but still need fast access to cash. Terms go as long as five years.

Why Avant is the best personal loan for people with bad credit: Avant specializes in lending to people with fair or poor credit. Most of its customers have credit scores between 600 and 700.

Perks: You can get your money within one business day after you’re approved.

What to watch out for: Interest rates start at 9.95 percent APR and can go as high as 35.99 percent APR, which is higher than interest rates from other lenders. Avant also charges an administration fee of up to 4.75 percent and a $25 late fee.

4. Marcus by Goldman Sachs

Overview: Interest rates on personal loans from Marcus start as low as 6.99 percent, and you can borrow as much as $40,000.

Why Marcus by Goldman Sachs is the best personal loan for debt consolidation: Marcus specializes in debt consolidation loans with broad loan amounts and a relatively low APR cap of 19.99 percent. With a debt consolidation loan, you borrow money with one loan to pay off many smaller loans or credit cards that were charging much higher interest rates.

Perks: Marcus doesn’t charge any fees. Also, if you make 12 consecutive months of loan payments in full and on time, Marcus allows you to defer a payment for one month without incurring additional fees or interest.

What to watch out for: Marcus doesn’t list any specific credit score, income or debt-to-income ratio requirements to help you learn if you’re eligible, and it doesn’t allow co-signers.

5. Best Egg

Overview: Best Egg offers personal loans for a variety of purposes, whether it’s debt consolidation, credit card refinancing, family needs or home improvements. Loans start at $2,000, and you can borrow as much as $50,000.

Why Best Egg is the best personal loan for low APRs: Best Egg’s interest rates start as low as 5.99 percent APR for those with the best credit. At 29.99 percent, its rate cap is roughly 6 percentage points lower than that of some lenders profiled on this page.

Perks: There are no prepayment penalties for paying your loan off early.

What to watch out for: Origination fees range from 0.99 percent to 5.99 percent, and $15 late payment fees are charged within three days of a missed payment.

6. Upgrade

Overview: Upgrade personal loans range from $1,000 to $50,000. You can use your personal loan for nearly anything, including debt consolidation, home improvement or a major expense.

Why Upgrade is the best personal loan for fast funding: You can get your funds within one business day after approval with an Upgrade loan.

Perks: Terms of two to seven years let you pay off your loan on a schedule that’s best for your budget. Interest rates start at 5.94 percent APR as long as you have strong credit to qualify.

What to watch out for: All personal loans come with a 2.9 percent to 8 percent origination fee. There’s also a $10 failed payment fee

7. Payoff

Overview: Payoff loans are specifically for borrowers who want to pay off high-interest credit card debt. If you’re struggling to get out of credit card debt and facing mounting interest rates, you can use a Payoff loan to get rid of it and then make fixed monthly payments to your one Payoff loan.

Why Payoff is the best personal loan for paying credit card debt: While the average rate for credit cards currently hovers around 16 percent, Payoff loans start at 5.99 percent, which could save borrowers money on interest and help them get out of debt faster.

Perks: Payoff gives you access to your free FICO score, updated monthly. There’s no penalty for paying your loan off early or making additional payments. There are also no late payment fees or fees if you have a returned check.

What to watch out for: You’ll need to have a credit score of at least 640 to qualify. There’s an origination fee of up to 5 percent.

8. Upstart

Overview: You can borrow as little as $1,000 and as much as $50,000 with an Upstart personal loan. Loans come with three- or five-year terms and APRs from 6.95% to 35.99%

Why Upstart is the best personal loan for little credit history: While Upstart has minimum credit score requirements, it evaluates more than just your credit score when you apply. The lender looks at your education, your job history and some credit score factors when determining your eligibility.

Perks: You can apply even if you don’t have a long credit history. If you’re relatively new to borrowing money, you might be eligible. Also, there’s no prepayment penalty for paying your loan off early.

What to watch out for: Co-signers aren’t allowed, and Upstart charges an origination fee of up to 8 percent and a late fee that’s the greater of $15 or 5 percent of the payment due.

9. LendingClub

Overview: LendingClub’s rates range from 8.05 percent to 35.89 percent on loans of $1,000 to $40,000. Terms of three or five years are available.

Why LendingClub is the best personal loan for using a co-borrower: If you’re struggling to find a lender that will let you borrow, you might need to enlist the help of a co-borrower. Not every lender offers the option to do this, but LendingClub lets you submit a joint application to help you qualify for a loan or get a better interest rate.

Perks: There’s a 15-day grace period in case you can’t pay your loan the day it’s due.

What to watch out for: It takes around four days to receive your funds. There’s also an origination fee ranging from 3 percent to 6 percent.

10. PenFed

Overview: You don’t need to go with a traditional bank or an online lender to find the best deals. Credit unions also offer personal loans. While PenFed is geared toward military and service members, there are other ways to become a member.

Why PenFed is the best personal loan for small loan amounts: You can get a PenFed personal loan for as little as $600, which is ideal if you don’t need a lot of cash and don’t want to incur much debt.

Perks: APRs start at 5.99 percent, and there’s no origination fee or prepayment penalty.

What to watch out for: You’ll need to become a member of PenFed before receiving a personal loan. While anyone can become a member — you just have to maintain a $5 savings account with the company — it’s still an extra step in the process that could be a deal breaker.

Is Citizens Bank Any Good?

Citizens Bank should appeal to most banking consumers who want a traditional banking experience. It may be a good option for people who want to:

- Bank at a traditional brick-and-mortar location

- Access loan services such as student loans, home loans, or personal loans

- Access wealth management and investment services

- Have 24-hour online banking access

Citizens Bank offers the following types of accounts:

- Checking accounts

- Savings accounts

- Certificates of deposit

- Money market accounts

- Credit cards

Other Financial Products From Citizens Bank

- Personal loans

- Home loans and lines of credit

- Mortgage refinancing

- Student loans and refinancing

- Investing and insurance

- Retirement planning

- Wealth management

- Business banking

It offers all of the traditional banking services such as checking accounts, savings accounts, and loan services. With an easy-to-navigate site and app, you’ll be able to find all the information you need easily.

Compared to online-only banks, Citizens Bank’s interest rates are quite low. If you want higher rates of return on your savings and checking accounts—and don’t mind sacrificing the in-person service experience—then an online-only bank may be right for you.

Citizens Bank Personal Loan Calculator

Use this calculator to look at a variety of possible loans. Change your monthly payment, loan amount, interest rate or term. Press the “View Report” button to see a complete amortization schedule, either by month or by year.

To check the status of a Student Loan or Education Refinance Loan application, you may log into your account. If you would prefer to call in to speak with one of our Student Lending Specialist for more information on your application, you may call 800-708-6684. The Education Finance Department is open from Monday – Friday, 8:00 AM – 9:00 PM EST, and Saturdays from 8:30 AM – 5:00 PM EST.

Citizens Bank Personal Loan Phone Number

On the phone. Online. In Branch. When you need them, they’re here to help. For general questions please call us at 1-800-922-9999.

To get you to the appropriate area most efficiently, please use the best number below:

Business Banking

Hours: 7:00 AM to 7:00 PM Mon-Fri and 9:00 AM to 6:00 PM Sat, Closed on Sunday

1-800-862-6200 for existing business banking customers.

1-800-4BUSINESS for new customers.

Checking and Savings Accounts

Hours: 7:00 AM to 10:00 PM Mon-Fri and 9:00 AM to 6:00 PM Sat & Sun

1-877-360-2472 for questions regarding opening a new checking account, savings account, or a new CD.

1-800-922-9999 for questions about your existing checking account, savings account or CD.

Credit Cards

Hours: 7:00 AM to 10:00 PM Mon-Fri and 9:00 AM to 6:00 PM Sat & Sun

Citizens Card Services®

1-888-333-5145 for questions about credit card applications.

1-800-684-2222 for questions about your credit cards.

Home Borrowing

Hours: 8:00 AM to 8:00 PM Mon-Thurs, 8:00 AM to 6:00 PM Friday, 9:00 AM to 3:00 PM Saturday

Citizens Home Equity Loans® Customer Service

1-800-340-5626 for questions regarding an application for a new home loan.

1-866-999-0216 for questions about an existing home loan.

Citizens Mortgage Loans® Customer Service

Hours: 8:00 AM to 8:00 PM Mon-Fri

1-888-514-2300 for questions regarding new mortgage applications.

1-800-234-6002 for mortgage servicing / existing mortgage customers.

Personal Loans

Hours: 8:00 AM to 7:00 PM Mon-Fri and 9:00 AM to 5:00 PM Saturday

Citizens Personal Loans®

1-888-333-0104 for questions about personal loan applications.

1-866-999-0107 for questions about your personal loans.

Student Lending

Hours: 8:00 AM to 9:00 PM Mon-Fri and 8:30 AM to 5:00 PM Sat

Citizens Student Loan® Customer Service

1-800-708-6684 for questions about your student loan applications.

1-866-259-3767 for questions about your student loans.

Citizens Education Refinance Loan® Customer Service

1-888-411-0266 for questions about your education refinance loan applications.

1-866-259-3767 for questions about your education refinance loans.

Investing and Retirement

Hours: 8:00 AM to 6:00 PM Mon-Fri

1-866-919-4520 for Citizens Securities, Inc.℠ existing investment and retirement accounts

1-866-471-5465 for SpeciFi® digital advisor enrollment assistance or account inquiries

1-866-919-7699 for Citizens Premier Advisory™ or automated account inquiries

1-866-605-4357 for Clarfeld | Citizens Private Wealth™ or automated account inquiries.

Citizens Bank Student Loan Reviews

Citizens Bank offers two refinancing options: one for loans in the student’s name, and one for loans in the parent’s name. Both are good for existing Citizens customers, as the lender offers a 0.25 percentage point interest rate discount for borrowers who have a qualifying account with the bank.

Beyond that, refinancing through Citizens Bank is a solid option for students who are financially stable but didn’t graduate, as well as non-U.S. citizens with a qualifying co-signer. It’s less ideal if you want to take over your parents’ loans. Citizens’ process is more complex than with other lenders: Your parent needs to refinance first with you as a co-signer, then you can apply to refinance on your own.

Interest rates, fees and terms

- Soft credit check to qualify and see what rate you’ll get: Yes.

- Loan terms: 5, 7, 10, 15 or 20 years.

- Loan amounts: $10,000 to $500,000.

- Can transfer a parent loan to the child: Yes, but the parent must refinance the loan first with the student as a co-signer.

- Application or origination fee: No.

- Prepayment penalty: No.

- Late fees: Yes; 5% of payment amount for payments not made within 15 days of the due date.

Requirements

Citizens Bank doesn’t disclose most details about what it takes to qualify for student loan refinancing. Lenders typically look for borrowers who have good credit and enough income to afford their debts and expenses.

Financial

- Minimum credit score: Did not disclose.

- Minimum income: $24,000.

- Typical credit score of approved borrowers or co-signers: Did not disclose.

- Typical income of approved borrowers: Did not disclose.

- Maximum debt-to-income ratio: Did not disclose.

- Can qualify if you’ve filed for bankruptcy: Did not disclose.

Other

- Citizenship: Eligible noncitizens can qualify with a U.S. citizen or permanent resident co-signer.

- Location: Available to borrowers in all 50 U.S. states.

- Must have graduated: No.

- Must have attended a school authorized to receive federal aid: Yes.

- Percentage of borrowers who have a co-signer: Did not disclose.

Citizens Bank Student Loan

Unexpected or large expenses, like books, computers, extra tuition, and travel, can come up during any semester. Private loans help fill the financial gap after you’ve exhausted all of your other financial resources, including grants, scholarships and federal loans.

Unexpected or large expenses, like books, computers, extra tuition, and travel, can come up during any semester. Private loans help fill the financial gap after you’ve exhausted all of your other financial resources, including grants, scholarships and federal loans.

Private loans, like our Citizens Bank Student Loan®, can give you the versatility to pay for all your education-related expenses and the flexibility to apply when you need the funding most.

Citizens Bank is a school-certified private loan option for undergraduate students attending eligible institutions at least half-time. Some of the benefits include:

- No application, origination or disbursement fees

- Easy, online application process

- Ability to be used with Stafford Loans

- Funds sent directly to the school

- Three repayment options

- An interest rate reduction when you sign up for an automatic payment deduction from any eligible Citizens Bank account

- Possible lower interest rates when you apply with a qualified cosigner

What Credit Bureau Does Citizens Bank Pull?

When applying for an unsecured personal loan, Citizens Bank primarily will pull information from Equifax. If there is information unable to be verified within a person’s Equifax credit file, Citizens Bank may request information from one of the other two major Credit Bureau’s (Experian, Transunion).

How do I Increase my Credit Limit With Citizens Bank?

The only way to request a credit increase with Citizens Bank is by phone; they do not offer online requests. If you need guidance through this process, you can also stop into your local Citizens Bank branch, where an employee can help you through the process.

Before you decide to request a credit limit increase, it’s important to note that Citizens Bank does run a hard inquiry on your credit report, which can negatively impact your credit score. This is particularly true if you have recently applied for credit cards or credit limit increases with other companies.

To request a Citizens Bank credit limit increase, follow these steps:

- Call the Citizens Banks Credit Card Services line at 1-800-684-2222, and when prompted, press “1” for account information.

- Enter your 16-digit credit card number and complete the automated authentication process. If you do not have your credit number, you may be able to authenticate by entering your Social Security number; however, please note that you will be required to provide one of these numbers in order to move forward with a credit limit increase request.

- Once you’ve authenticated through the automated system, you will be placed in a queue until the next representative becomes available.

- Inform the representative that you would like to request a credit limit increase.

- In order to begin the application, the representative will need to ask a series of questions regarding basic verification information; this may include your name, address, credit card number, Social Security number, etc.

- Additionally, you will also be required to provide information about your finances, specifically your income and monthly housing expenses.

- Upon providing the answers to these questions, the representative will submit your application, and, unless you have further issues to discuss, the call will come to an end. Decisions are not immediate.

Credit limit requests are processed within seven to ten days and communication of a decision is sent out via mail; however, customers can also contact the Citizens Bank Credit Card Service department via phone within the seven-to-ten-day window to inquire about their application.

If approved, you will receive a letter alerting you to this decision as well as your new credit limit. If denied, you will receive an explanation from customer service about why you were denied.

Does Citizens Bank Have a Credit Card?

Citizens Bank offers different personal credit cards. If you decide you are interested in applying, you may apply online, at a branch, or you may reach out to our Customer Direct Sales Team at 1-877-360-2472. They are available from Monday – Friday, 8:00AM to 9:00PM and Saturdays and Sundays 8:00AM to 8:00PM EST.

The process of applying for a credit card can be pretty quick and easy — if you know what to expect. In many cases you’ll know if you’ve been approved or declined instantly. If you’re interested in applying for your first credit card, follow the steps below.

Step 1: Before you apply

The process of applying for a credit card should start well before you click “submit” on your application. Taking the time to understand your credit profile will leave you with a better understanding of the offers you’re eligible for, and/or what you need to do to improve.

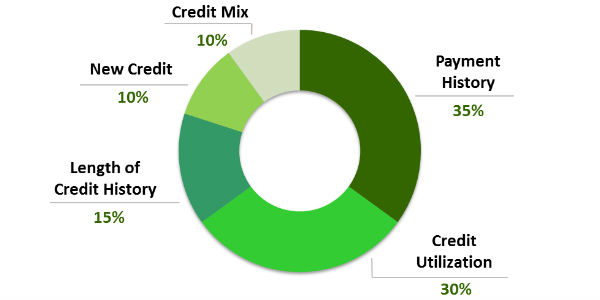

- Know your credit score. Your credit score is determined by five factors:

- You can have multiple credit scores since lenders use different credit scoring systems like FICO or Vantage. Free VantageScores are available from apps like Credit Karma or Nerd Wallet.

- Review your credit history. You get to review a free report every 12 months from each of the three major credit bureaus — Experian, Equifax, and Transunion. Go through these reports and make sure everything is accurate. Identity theft happens. Dispute anything that looks incorrect directly with each bureau in order to safeguard your credit.

- Record your income and employment history. Credit card issuers want to be sure you can make the payments; so they may ask how much you make and how long you’ve been employed. Gather this information and keep it on hand.

Step 2: Find the card that’s right for you

Now that you have a solid picture of your credit situation, you’ll need to decide which card is right for you. Consider your credit habits before choosing which credit card you should get. Do you carry a balance from month to month? Consider a card with low interest. Do you consistently make full payments? Look at rewards cards that can help you optimize your cash flow.

Remember to read through the terms and conditions so you can compare your options. Fees and interest rates are important deciding factors when choosing a credit card. Having no annual fees might not be worth it if the card has a high interest rate. Think through your financial situation, and determine your priorities.

Step 3: Complete the application

Filling out the actual credit card application is likely the easiest part of the process. You typically have the option of applying over the phone, in person, or online. Online is going to be the quickest and easiest method, since a lending decision is often made instantly.

To apply, you will need the following information:

- Your full name

- Social Security number

- Date of birth (must be at least 18)

- Current address

- Annual income

- Current employer/length of employment

Pro tip: Keep your information safe! Never fill out an application on public Wi-Fi or through an unsecure connection.

Step 4: Lending decision

Once your application is submitted, one of three things will happen. It will be approved, submitted for further review, or denied.

If your application is approved, congratulations — you should expect to receive your new card in the mail within a couple of weeks. Use it wisely.

If further review is requested, then the credit card company wants to take a little more time deciding. At that point they should provide you with a time frame in which you can expect to hear a decision.

If your application is denied, then you should expect to receive an “adverse action notice” explaining the reason. Although you might be frustrated with this news, always read through the notice to understand what you need to improve or if there was a mistake on your application. Typos happen.

Even if you were denied, all is not lost. You can improve your credit by applying for a secured card, which requires a security deposit. You can also ask a parent or spouse about becoming an authorized user and “piggybacking” on their credit to help build-up your own.

How Much Can I Withdrawal From ATM Citizens Bank?

The minimum amount you may withdraw at a Citizens Bank ATM is $20.00. If you need to make a withdrawal less than $20.00, you may absolutely step in to your local branch for assistance.

Read Also: Top 5 Best VA Loan Lender

Each Debit Card will have a daily ATM withdrawal limit as well as a daily limit for purchases made via Debit/Credit. These limits vary from account to account and are not impacted by traveling abroad. Most account types will indeed support a $500 per day ATM withdrawal, however, it’s always best to check your personal limits.

If you’re interested in your daily limits, please don’t hesitate to contact our Customer Service Team at 1-800-922-9999 or conveniently chat with us! Our Customer Service Team is available for you 24 hours a day, 7 days a week and our Live Chat Team is available for you Monday-Friday from 8:00AM – 8:00PM EST, Saturday from 8am-430pm EST, and Sunday from 8:30AM-5:00PM EST!

To chat with them, please visit their customer service page and then click Chat with Us. Doing so will begin a live chat interaction with a Specialist who would be glad to confirm your Debit Card daily limits and adjust them for you as needed!

How do I Redeem my Citizens Bank Reward Points?

You may view/redeem your rewards by logging into Credit Card Online. Note that you are eligible to redeem your rewards in increments of $25 in cashback. The Reward Points may be redeemable as a deposit into your Citizens Bank Personal Deposit Account or a Statement Credit.